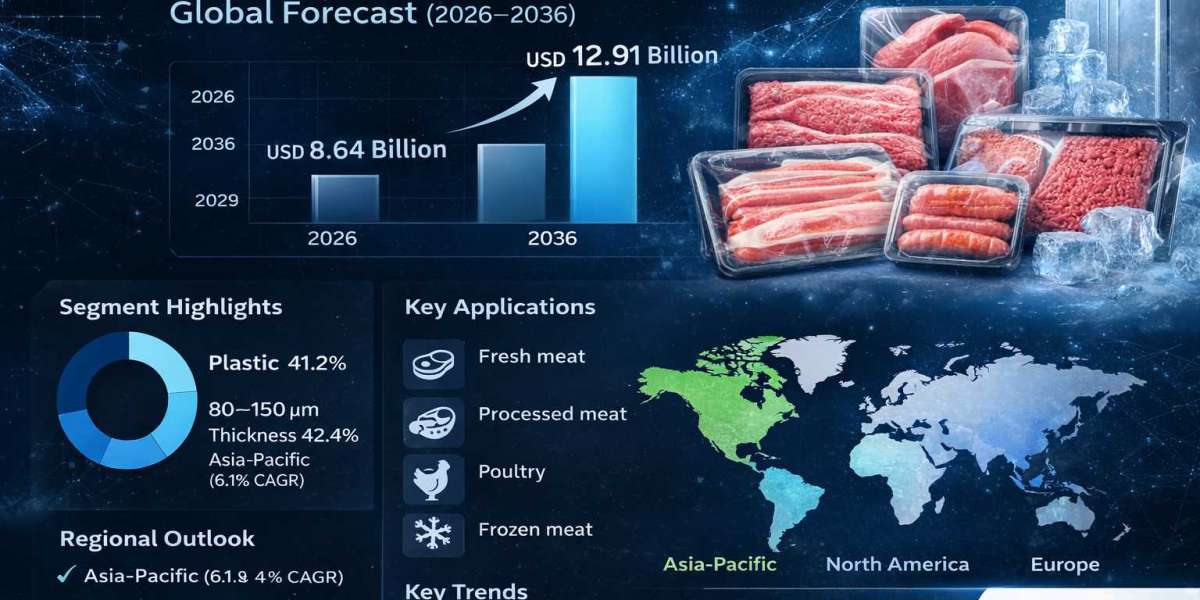

The global meat packaging market continues to expand steadily as demand for safe, durable, and shelf-life-extending packaging formats rises across modern retail and food processing industries. The market was valued at USD 8.30 billion in 2025 and is estimated to reach USD 8.64 billion in 2026. According to industry analysis, the market is projected to grow to USD 12.91 billion by 2036, registering a CAGR of 4.1% during the forecast period.

Quick Stats: Meat Packaging Market (2026–2036)

- Market Value (2026): USD 8.64 Billion

• Forecast Value (2036): USD 12.91 Billion

• CAGR: 4.1%

• Leading Segment: Plastic Material (41.2% Share)

• Key Product Segment: 80–150 µm Thickness Packaging (42.4% Share)

• Fastest-Growing Countries: India, China, Canada, United States, Spain

• Key Growth Driver: Expansion of cold chain logistics and rising demand for vacuum and MAP packaging

Structural Growth Driver: Cold Chain Expansion and Food Safety Compliance

One of the most important structural drivers in the meat packaging market is the global expansion of cold chain infrastructure. As chilled and frozen meat distribution networks expand across emerging economies, the demand for high-barrier packaging solutions capable of controlling oxygen and moisture ingress continues to grow. Packaging formats designed for vacuum and modified atmosphere systems are essential to maintaining product quality, extending shelf life, and reducing spoilage during transportation.

Key regulatory and industry frameworks include:

- Food-contact safety regulations for packaging materials

• Packaging recyclability and waste reduction policies

• Extended Producer Responsibility (EPR) compliance frameworks

• Retail sustainability scorecards and supplier qualification standards

• Packaging performance standards for vacuum and MAP systems

From Compliance to Industry Transformation

The meat packaging industry is moving beyond basic compliance toward structural transformation driven by sustainability, operational efficiency, and supply chain resilience. Packaging suppliers are increasingly collaborating with meat processors and retailers to develop solutions that combine high barrier performance with recyclability and reduced material usage.

Companies in the market are prioritizing:

- Sustainability performance and recyclability targets

• Cost efficiency and material optimization

• Barrier performance for shelf-life extension

• Compatibility with automated processing lines

• Supply chain reliability and traceability

Technology Transformation: Advanced Barrier Film Innovation

Technological innovation remains central to the evolution of the meat packaging industry. Packaging converters are investing heavily in advanced barrier films and multilayer structures that enhance protection against oxygen and moisture while enabling recyclability improvements.

New developments in material science and converting technology are enabling manufacturers to reduce packaging thickness without compromising puncture resistance or seal integrity. Additionally, innovations in sealant layers and recyclable high-barrier films are helping the industry transition away from complex multi-material laminates toward simplified mono-material packaging systems.

Key innovation areas include:

- Advanced barrier film development

• Automation integration in packaging lines

• Lightweight and downgauged packaging design

• Sustainable and recyclable material engineering

• Manufacturing efficiency improvements in film converting

Segment Highlights

By Material Type

- Plastic (41.2% share): Dominates the market due to excellent barrier properties, sealing reliability, and cost-efficient converting processes used in vacuum and MAP packaging.

• Paper Paperboard: Increasing adoption in secondary packaging and eco-friendly solutions for processed meat products.

• Aluminum Foil: Provides superior oxygen and moisture barriers for specialized packaging formats.

• Biodegradable Compostable Materials: Emerging segment driven by sustainability regulations and retailer commitments.

• Glass and Metal: Used mainly for niche processed meat packaging applications.

By Thickness

- 80–150 µm (42.4% share): The most widely used range, balancing durability, flexibility, and sealing performance for vacuum bags and flexible films.

• Below 80 µm: Lightweight solutions for cost-efficient packaging applications.

• 150–250 µm: Used in heavy-duty packaging requiring higher puncture resistance.

• Above 250 µm: Specialized applications in rigid or semi-rigid packaging formats.

Regional Outlook: Emerging Economies Drive Adoption

The global meat packaging market shows strong regional variation, with emerging economies driving most of the volume growth while mature markets focus on compliance-led packaging redesign and performance upgrades. Asia Pacific remains the fastest-growing region due to expanding modern retail networks, rising meat consumption, and increasing cold chain investments.

- India (6.7% CAGR): Cold chain expansion and growth of organized retail drive demand for high-barrier packaging.

• China (5.4% CAGR): Online grocery and large-scale meat distribution networks increase packaging performance requirements.

• Canada (3.8% CAGR): Growth driven by retail consolidation and sustainability-focused packaging redesign.

• United States (3.7% CAGR): Replacement demand for advanced vacuum and MAP packaging technologies.

• Spain (3.5% CAGR): Export-oriented meat processing sector supports demand for durable packaging formats.

Risk Landscape: Market Constraints and Challenges

Despite steady growth, the meat packaging market faces several structural risks related to material costs, supply chain pressures, and regulatory complexity. Volatility in resin and aluminum prices can significantly impact packaging manufacturing costs, while recyclability regulations require substantial investments in material redesign and compliance systems.

Key market challenges include:

- Raw material price volatility

• Supply chain disruptions for packaging materials

• Infrastructure gaps in cold chain logistics

• Regulatory complexity in food-contact packaging

• High manufacturing and compliance costs

Competitive Landscape: Key Market Players

The meat packaging market is moderately consolidated, with global packaging companies leveraging advanced barrier film technology, large converting networks, and strong relationships with meat processors and retailers. Competitive advantage often comes from proprietary film formulations, material innovation capabilities, and the ability to meet evolving sustainability requirements.

Top key companies include:

- Amcor plc

• Berry Global Group, Inc.

• Winpak Ltd.

• Smurfit Kappa plc

• Sealed Air Corporation

Other notable companies include Faerch A/S, Constantia Flexibles Group GmbH, Mannok Pack, Bolloré Group, and SP Group.

Outlook: Future of the Meat Packaging Market

The future of the meat packaging market will be shaped by sustainability goals, technological innovation, and evolving food safety standards. As retailers and regulators push for recyclable packaging solutions, manufacturers will continue to invest in high-performance barrier films that maintain shelf life while meeting circular economy requirements.

Key future growth drivers include:

- Technology advancement in barrier film materials

• Sustainability initiatives and recyclability targets

• Manufacturing expansion in emerging economies

• Supply chain innovation and cold chain development

For an in-depth analysis of evolving industry trends and to access the complete strategic outlook for the market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/meat-packaging-market